January Fund Performance

Growth is now cyclical?

See below month end fund performance data ranked by monthly performance.

HOUSEKEEPING

If you want to read this on another site with interactive tables that you can click through on, click below:

Seriously, it’s much nicer - CLICK HERE

If you are receiving this via email, I suggest clicking the link and reading directly on Substack. The email formatting does not translate well and the information may appear as clipped or truncated in your inbox due to the size and length of the Substack post.

If this forwarded to you, feel free to respond to the Substack email or just send a sign up request on mrquick@substack.com or contact@ausyield.com.au

All tables are sorted by 1-month performance, with benchmark rows highlighted where relevant.

Data is current as of end-January 2026.

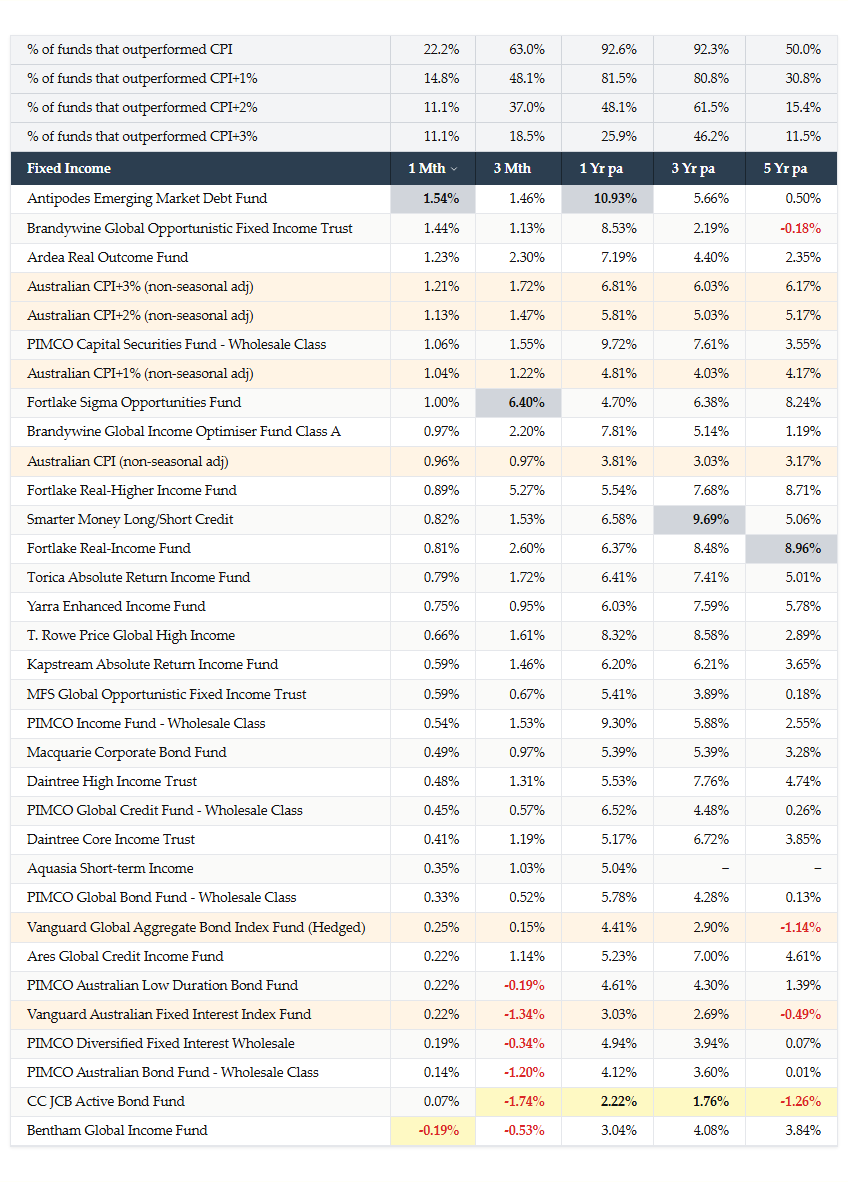

Fixed Income

Utterly insane month. Inflation comes in hot, CPI almost 4% for the year. Rates get priced in and back end of the Aus curve takes off.

At the same time, credit spreads continue to narrow as rate cut cycle continues in the US.

So credits continue to do OK (but for how long?) and bond funds get hammered again.

Only half the funds on this list outperformed CPI over 5 years.

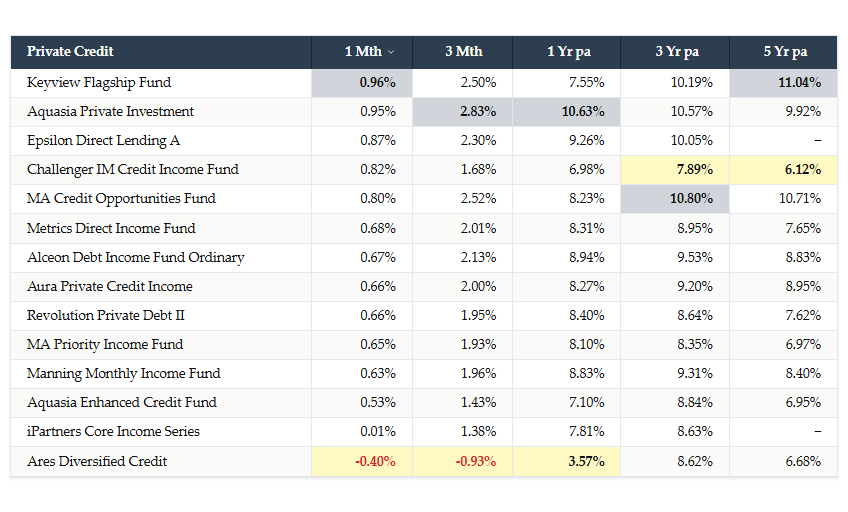

Private Credit

Rates taking off again. how many of the domestic players have exposures that are challenged in a rate rising cycle.

How many loans underwritten with a view for lower rates?

And how many loans extended with a view that rates fall making serviceability easier.

Private credit-ish, but my favourite exposure (Aussie RMBS) is going to start getting crowded. New funds galore, Revolution, Metrics, who else?

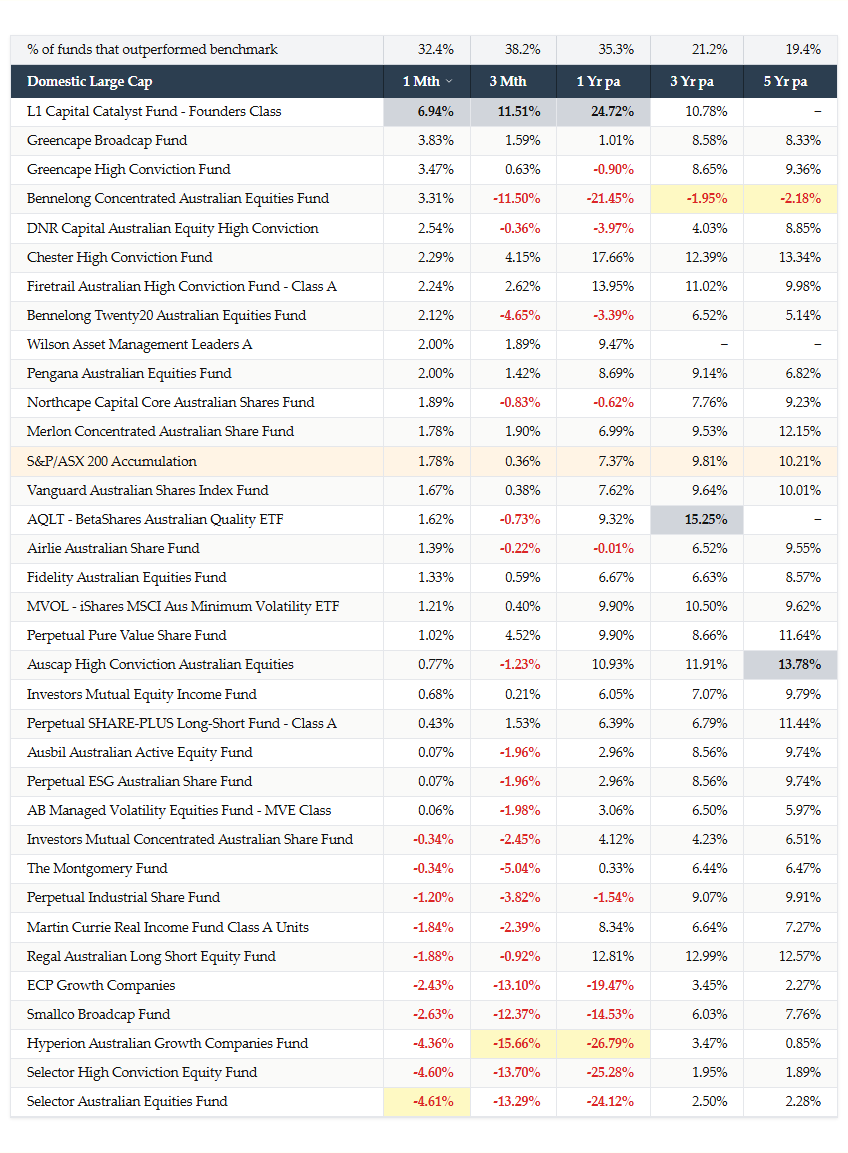

Domestic Large Cap

Horrific period for active management, only 10% of this list outperformed the index over 3 years!. Utterly insane numbers.

Think about all the active managers underweight CBA, at some point they will all go market weight. The flow of capital that remains outstanding is utterly gigantic

Bennelong with negative 5 year returns now. Over a 10%pa delta against the benchmark, utterly phenomenal capital destruction.

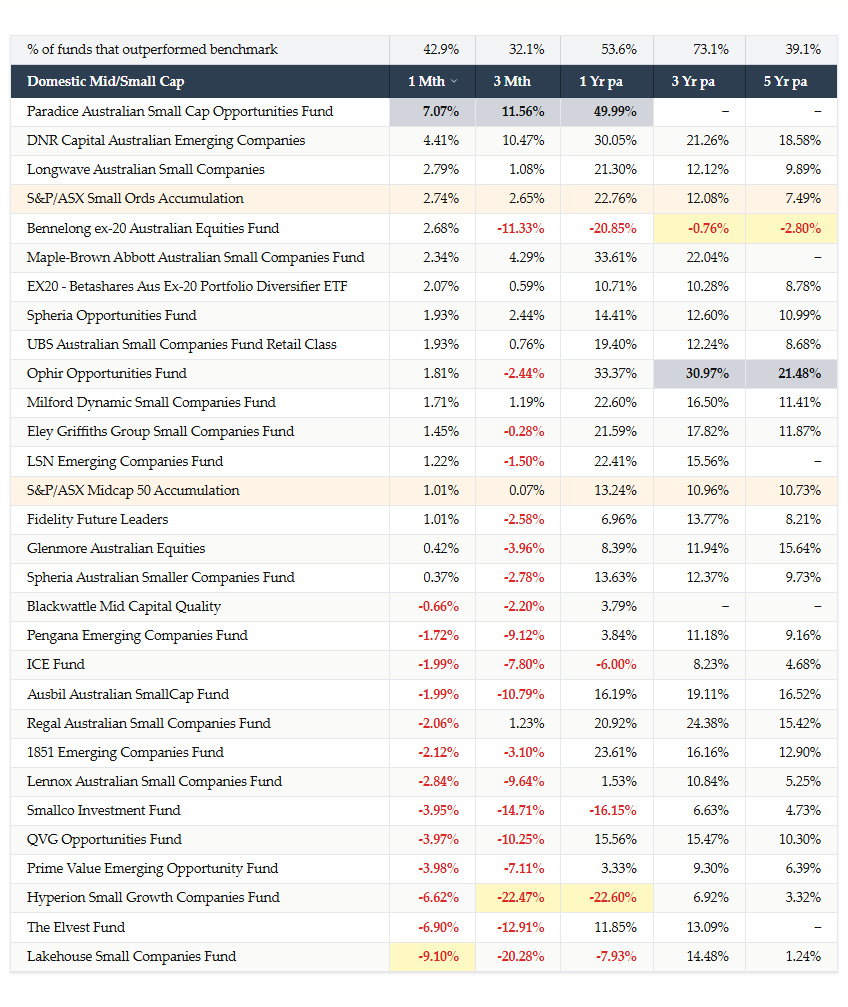

Domestic Mid/Small Cap

Some feral numbers at the bottom of the list again. This is the tech blow-up coming through and the real hit that happened in Feb hasn’t even come through yet.

Bennelong must be happy, a fund beat them to worst performing over 1 year.

No harm, they still lost their investors money over 5 years in what was among the most slam dunk environments for small caps I’ve ever seen.

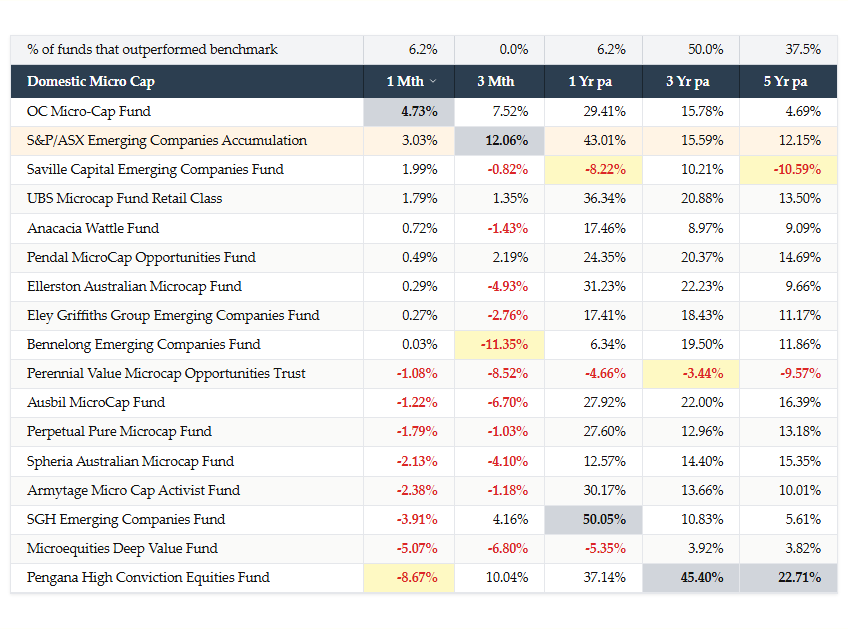

Domestic Micro Cap

Extremely rare seeing the benchmark beat every fund on the list!

Gold and Lithium driving this end of the market, Feb numbers will show that reality struck back.

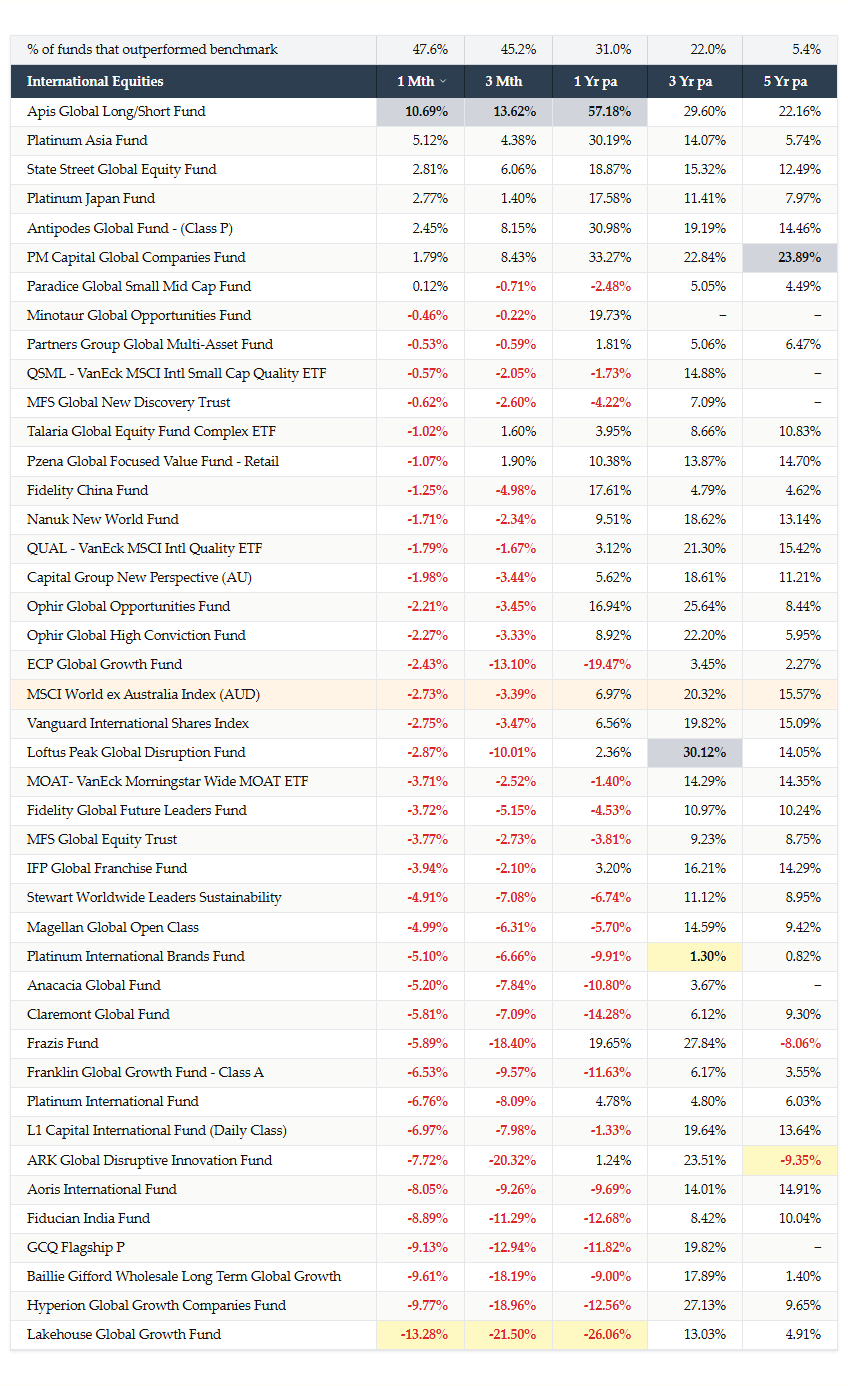

International Equities

6% of funds outperformed their benchmark over 5 years.

Index was up 13% over the year yet 45% of funds covered here managed to lose money over 12 months. WHAT.

The quality bubble continues to deflate.

One of my more uncomfortable ideas is that quality factor works from here on in, I feel disgusting saying it. Though not enough of these funds have been hit by redemptions to say that yet.

Okay I will stop banging on about active management indirectly. Directly, the passive has smashed active management.

I’m calling it, active management time is now. You don’t get that level of underperformance persistently, most of the underlying companies will generate good earnings and the recent vol will likely mean financials for many will improve.

Furthermore, AI will get implemented in many businesses, there will be winners within the Tech/SaaS group.

So many people were warning of a sell-off. Well its here, what is your plan? Climb the wall of worry and allocate to a manager who can navigate the vol and allocate to beaten down companies that can persist?

What’s that? Active managers that look for “quality” and have a decent understanding of the current market environment? Some kind of oversold active manager(s) with a quality bias? Hmm...

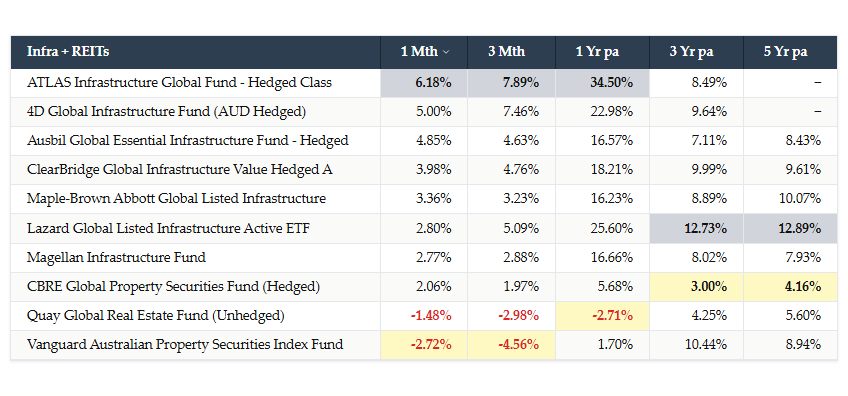

Infra + REITs

Rates falling globally, infra managers do well.

Rates rising in Aus, Aus property does poorly.

Not rocket science, its all duration.

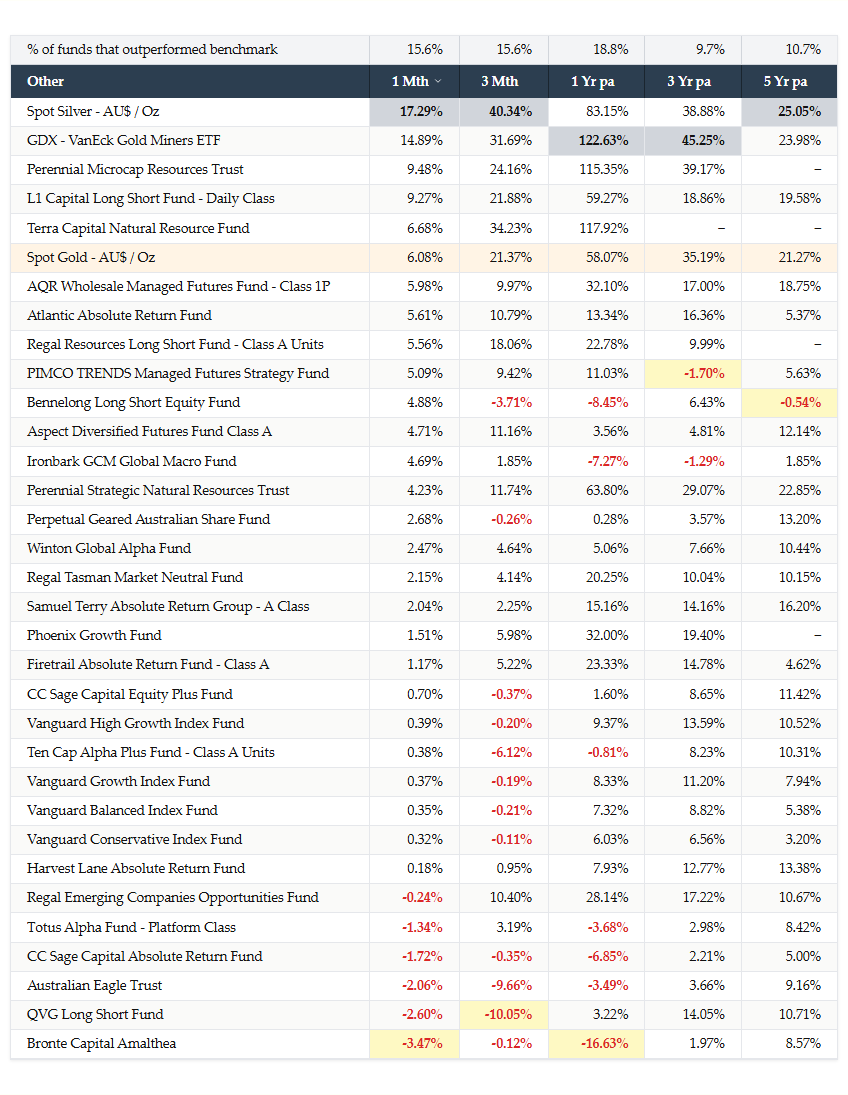

Other

Ignore Silver here, got obliterated in Feb so will be at the bottom of the list.

AQR, sweet baby jesus. Either Cliff Asness has truly become one of the great (US$100bn AUM) or there is mega equity risk coming through. Feb numbers suggest it isn’t just equity risk.

I remain perpetually frustrated I have no allocation here.

Don’t trust the Long Short fund numbers for Jan, they’ve all ripped back in Feb.

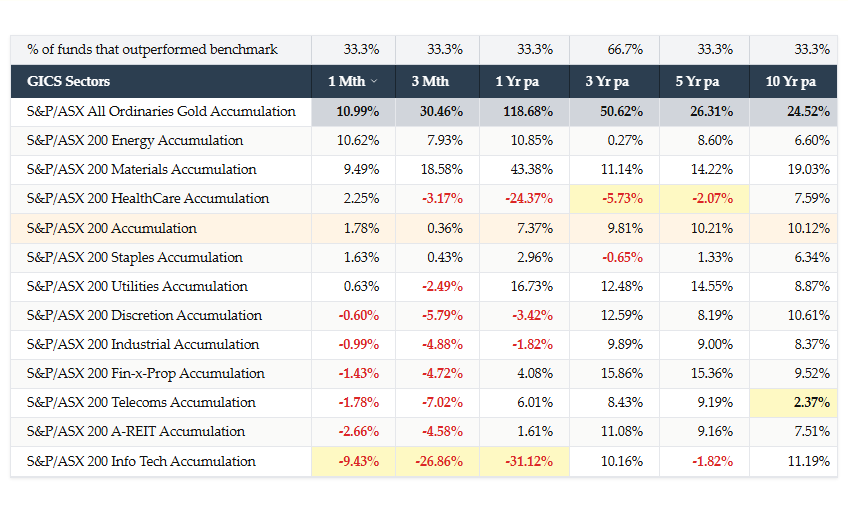

GICS Sectors

Tech will underperform Healthcare after February I think over the long run.

CSL trying its hardest to destroy the healthcare index now.

Is Aussie tech dead? More comments in the thoughts section.

I still find it fascinating that staples generated less than inflation like returns over 5 years and is the third worst sector over a decade.

Crypto

Huge negative numbers, negative returns over a year now.

For those that are interested, a bigger technological event is coming larger than AI in my view.

Quantum compute is not far away now. Q-Day will mark the event. By 2030 in my view.

Q-Day has the greatest monetisation event of all time, the ability to hack into a dormant BTC addresses and sell millions of Bitcoin. The ultimate payday.

Q-Day represents a gigantic risk. But how about I give you some gigantic upside too.

Bitcoin ETFs represent one of the biggest reflexivitiy trades of all time.

As of Jan, NASDAQ removed all position limits on crypto ETF options.

The moment is definitely not today, but at some point in the future we will have a moment where there will be extensive spot, ETF and futures buying, on top of which there will be an uncapped number of call options driving the crypto ETF market higher.

Long way to go, MSTR has to blow up and Q-Day will need to happen before we get to this stage.

Thoughts of the month

What to do after the SaaS sell-ff

From the outset, I’ll reiterate what I said about 2 months ago, Claude Code (and ChatGPT Codex) is the single most significant thing that has ever happened in my career.

The silly thing on my front is I should have been short tech names because in hindsight, if this affected me as someone who works in finance let alone tech workers, can you imagine the disruption in the tech sector? Well you don’t even need to imagine, ASX XIJ (-43%), ASX XTX (-37%) are representative of what happens if you’re exposed to “disruption” from AI. That is an utterly brutal drawdown in anyone’s book, to get back to evens, XIJ has to bounce +75% to get back to previous peaks.

Not in the realm of impossible but things have fundamentally changed so the question we must answer is, can we get back there?

Let’s actually try to answer this.

Feedback

I have spent the last few weeks talking to a few SaaS companies (CFOs, COOs, CTOs) about how they’re approaching AI and their views. The majority of these companies are private, I have a holding in some of them (which I think are now worth a lot less). Insights below:

All engineering teams are using Claude Code/ChatGPT Codex, I haven’t talked to a single person who said they haven’t incorporated this into their workflows. Existential crisis realised.

V: Personally, this is one of the most shocking things I’ve ever heard as the pace of adoption is ridiculous. But this also lends to the idea that investing in software dev tools is a mugs game, there is no barrier to entry and users are incredibly fickle.

V: On PA, obviously one of my bigger direct holdings as private SaaS is a devtool... ffs

I’ll quit digressing, when I’ve talked to CFOs the interesting thing is they can’t point out to efficiency just yet and still challenged to see how things work, some comments (non-verbatim obviously):

It has absolutely made everyone efficient

Everyone is doing more and are a bit more productive

Sales teams generate revenues, so picking up the phone calling people or meeting people hasn’t changed and this has a particular cadence – AI has done nothing to unlock value here

Engineering teams are cost centres

One question I posed is if they can do more, can it be turned into revenue

Answer is maybe; you can ship more stuff or improve outcomes but that doesn’t necessarily turn into revenue

Second question I’ve been asking is can you reduce headcount

Blatant answer is “no”

Surprisingly everyone I spoke to has already gone through the headcount exercise with absolutely 0 change

“You can fire someone but then I need someone to train the agent”

That is the main thing I kept hearing, you can’t really reduce headcount because engineering teams are treated as a cost centre – they’re already run as tight ships

V: This is perhaps reflective of the zero cost-of-capital era expiring and the last tech blow-up has already forced everyone to think about their economics and profitability more closely.

Perhaps reduction in headcount growth, but no direct benefit in headcount reduction. Yet...

The final bit of feedback is everyone recognises that the barrier for new entrants is significantly lower, that if a few sales people and some strong engineers got together, that any industry can be disrupted now

This lends to the final idea of although you won’t see revenues change all that much (in the near term) and perhaps there might be better profitability at SaaS companies, that the terminal values all need to be marked lower because the barrier for competition is just so much lower today.

So the direct answer is earnings haven’t fallen, this is another valuation recession for Tech just like 2022. Earnings haven’t gone anywhere but terminal values for every business is lower (for now?).

Noting that these are all <$500m Mcap, <$50m revenue companies so the caveat is headcount could be reduced at large companies that I haven’t picked up on quite yet.

The Playbook

Frankly I think AI is utterly existential if you’re a large tech company, but I still think large tech companies are better positioned to navigate who knows what than smaller ones because at the end of the day, it is all about sales.

How do we play this?

Need to risk weight it appropriately

Need to be aware that any new competitor for any listed company that gets any kind of traction will likely push around valuations significantly. One AFR article can easily halve Xero tomorrow if someone raised capital for an “AI Competitor”.

I think no change to fundamental earnings in the next 12 months – so an opportunity in this respect

The bull case is potential upside earnings revision due to potential headcount reduction

An outcome here is valuations might fall but earnings improve – there is a hedge there against each piece but unfortunately valuations are more volatile. Both risk and opportunity.

Allocating here is taking a bet that valuations bounce back from your entry point + earnings improve due to headcounts. Both scenarios plausible.

Picking bottoms (hehe) is challenging, there is still significant shareholder turnover in these companies.

On sale, everything is 50% off!

Imagine if a year ago someone told you that you could buy WTC, REA, TNE, CAR or PME at 30-50% off. Everything is on sale! Opportunities like this seldomly appear but need to climb the wall of worry and position appropriately, how much risk are you willing to take on? Are you ok if this goes down another ~50%? How much permanent capital destruction is ok?

If you’re looking at US stocks, stock-based compensation (SBC) is still a significant headwind.

I think it was Joe from Bloomberg’s Odd Lots (maybe, I can’t remember) who said something this week along the lines of - if terminal values are falling, and these SaaS companies are all negative free cash flow after SBC, then they have no earnings and no terminal value so its not a surprise they’re all falling.

I honestly don’t know what the final outcome is and neither does anyone, which is reflected in lower terminal values and lower valuations across the board. But I don’t think there is earnings erosion in the near term so the ultimate question is whether the market will reward this in again the future?

An idea you rent rather than own for now. Tech migrating to cyclicals.

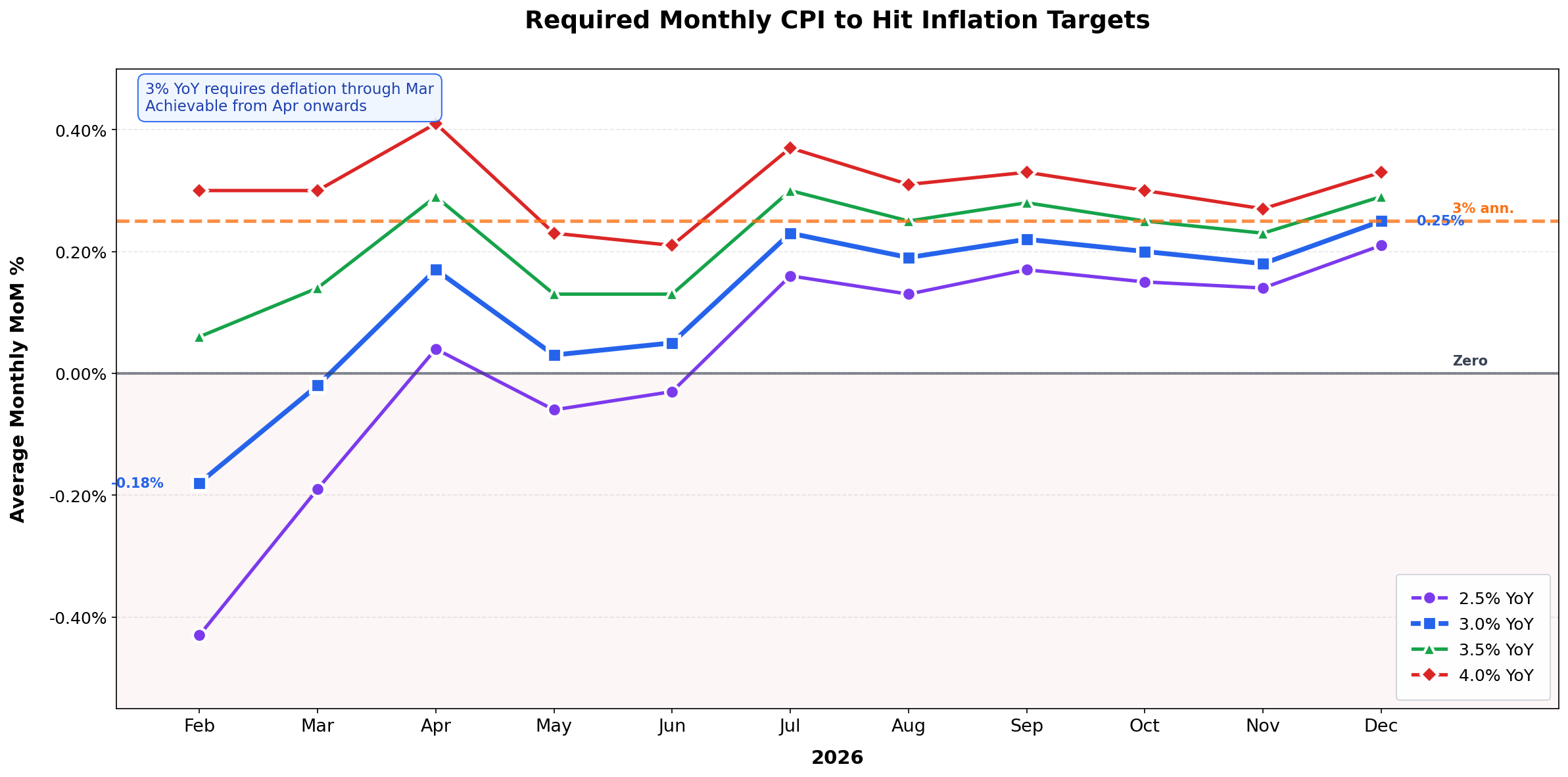

The Path to 3%

The RBA has moved to monthly CPI reporting, which is making forecasting a bit more fun for me as more granular data means you can work out which months are dropping out and what needs to happen to see for the annualised inflation rate to fall/rise.

To get back to target (let’s call it 3%), the below needs to happen:

To hit 3% annual inflation by March 2026, monthly prints need to average -0.02%. Deflation lol.

To hit 3% by June, need 0.05% per month. Achievable I guess, but that’s effectively flat/no inflation for six straight months.

To hit 3% by December 2026, need 0.25% per month. That’s a normal month in a 3% inflation world which i think is entirely achievable, especially with base effects helping in the second half of the year.

Trying to get to 3% by March is cooked because the Dec-25 spike pushed the index to 100.97. For March 2026 to print 3.0% YoY, the index needs to be 100.90, meaning the only path to 3% by March is three months of price declines. Yeah the price of petrol is helping (for now), but insurance and housing costs have continued to run higher.

March therefore is locked in around 3.5%-3.8% unless something utterly breaks. And likewise, June seems to be pinned around 3.8% annualised too.

December 2026 at 3% is achievable.

Predicting Inflation

No idea, if you think you have insight, so does a dart board.

But, we have data to work with, and the answer clearly is that before you give into the AFR doom headlines, it is mathematically challenging for inflation to drop below 3.8% through to June. Possible but we need some really helpful data.

One might even expect that towards the end of July when we get the June inflation data, that the concept of persistent Inflation is going to become a prevalent discussion point. This means by mid-July, if inflation stays around that 3.5%-3.8% range (highly likely), everyone is going to call the RBA fools and call for further hikes. There is a non-zero chance that an additional rate hike get priced into markets by the middle of the year in my view.

Will they hike or not? Who knows who cares but the data in the second half of the year is very supportive to inflation coming back towards the 3% target.

A chart to visualise below. 3% average inflation takes us through to over 3.5% inflation by the end of the year.

The headline figure in my view is not going below 3% until 2027 guys, buckle up.

Inflation - Bonus thought

There is a concept we haven’t discussed for a long long time because the West coast has been down in the dumps, but commodities are booming and Perth is printing money again. The old conversation of Australia having a 2-speed economy is going to kick in at some point. A mining boom combined with an (insert your reason) East coast economic slowdown.

We have forgotten what that is like, but Australia makes money in the West and we rely on migration to grow in the East. With immigration likely slowing down significantly from here, the RBA is going to remain challenged balancing the economy.

And unlike times of past, social media influence is a much bigger, meaning this will take a life of its own. Did you know “The Dominion League” won the 1933 WA Secession Referendum with a 2/3 Yes vote? Constitutionally unfeasible but the popularity was there.

When does the 2-speed economy strike?

Thanks

Well done for making it this far and it pleases me you are reading this sentence. I thank you for reading the above and I hope it has provoked some thoughts.