December Quarter Fund Performance

Cracks

Hi Everyone,

Stale data as this is December quarter data, but plenty of people have asked for it, so here it is!

Spent Jan moving back to Sydney, what a gorgeous city :) Though I do miss the peace and quiet of country NSW.

No thoughts this month, I have plenty but also have a lack of time. Jan update will come in 2 weeks time too.

Cheers,

V

See below quarter end fund performance data ranked by quarter performance.

HOUSEKEEPING

If you want to read this on another site with interactive tables that you can click through on, click below:

Seriously, it’s much nicer - CLICK HERE

If you are receiving this via email, I suggest clicking the link and reading directly on Substack. The email formatting does not translate well and the information may appear as clipped or truncated in your inbox due to the size and length of the Substack post.

If this forwarded to you, feel free to respond to the Substack email or just send a sign up request on mrquick@substack.com or contact@ausyield.com.au

All tables are sorted by 1-month performance, with benchmark rows highlighted where relevant.

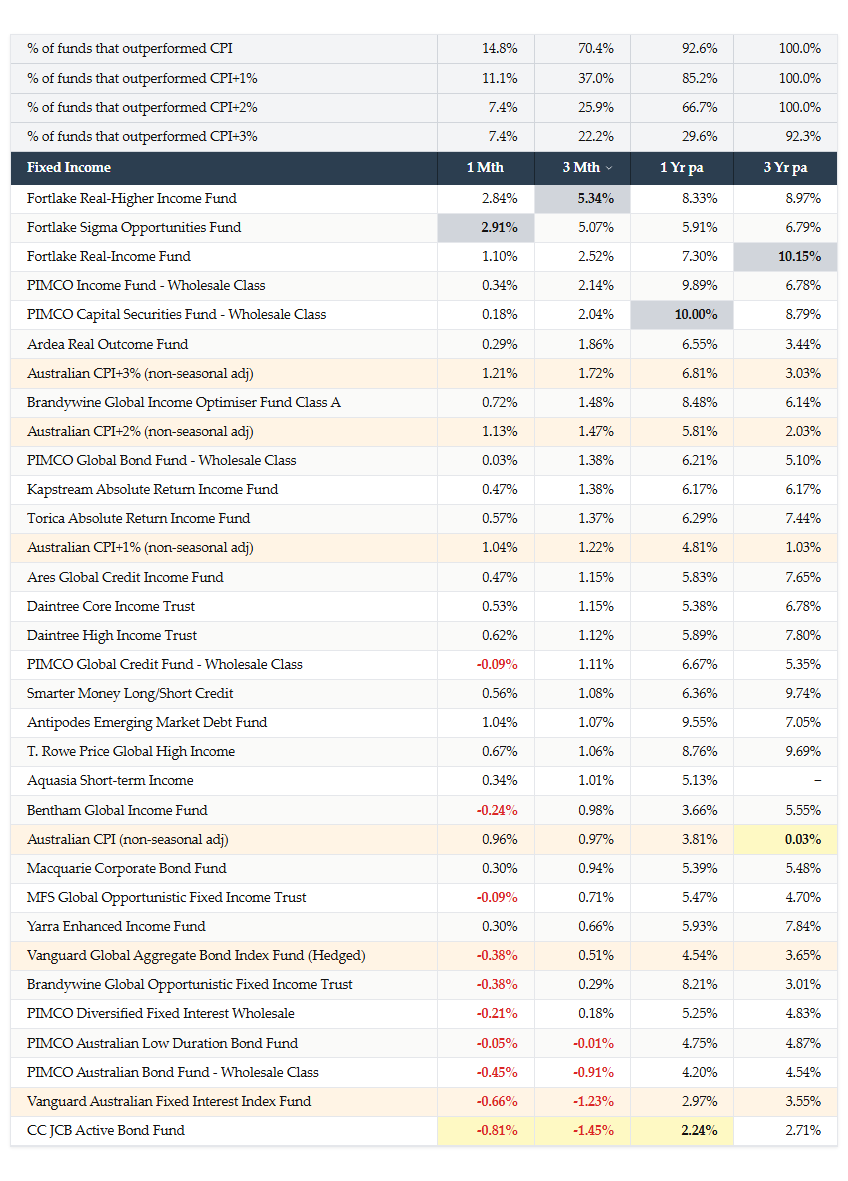

Fixed Income

Holding any kind of duration has meant that you underperformed inflation + 1-2%

Fortlake ripping back now! The alpha turns up slowly then quickly.

Credits have done well but credit spreads super duper narrow now.

We talk about equities being “overvalued” yet little to no commentary around spreads.

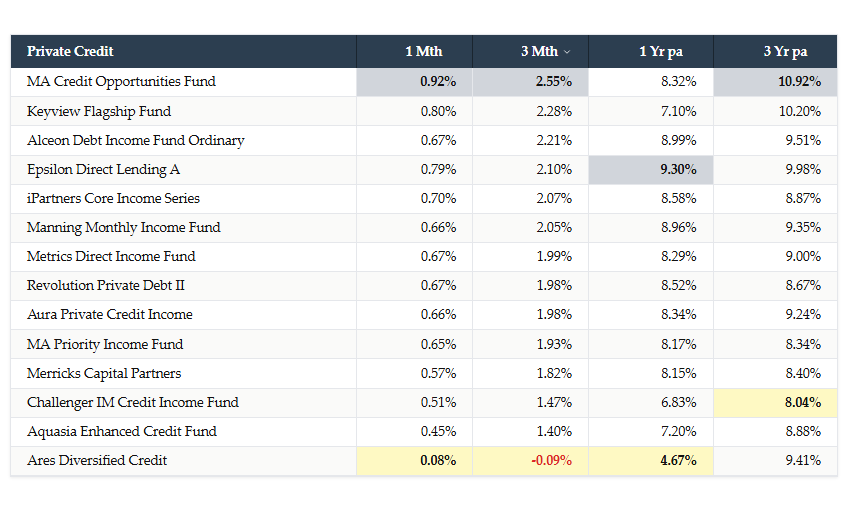

Private Credit - Domestic

I want to reinforce the fact that there is little difference in returns between public and private credits over 3 years.

How much above inflation or cash rate should these funds be earning?

Let’s flip it the other way, what is equity risk premium? 5%? 6%?

So if a fund generates a yield greater than 9-10%pa over the last 3 years, the question then becomes what kinds of risks are you taking to generate these returns?

How much return above cash do you deserve is a critical question to answer.

And part of the historical spread (which was high) was because of the lack of players in the market. ie, more borrowers than lenders.

But as more new funds and new captive capital vehicles (the LITs) come to market, you can expect margins, and therefore forward returns, to be a bit tighter than historically implied.

Domestic Large Cap

Utterly filthy quarter where less than half the funds outperformed the ASX200. The larger the miss, the more concentration in the fund, all part of the active management game.

1/5 funds outperformed the benchmark over 3 years, but how much of that is YFYS flows driven and these PMs managing that risk?

What will come first? Will the YFYS tail end up wagging the dog or will APRA screw their head on about performance testing?

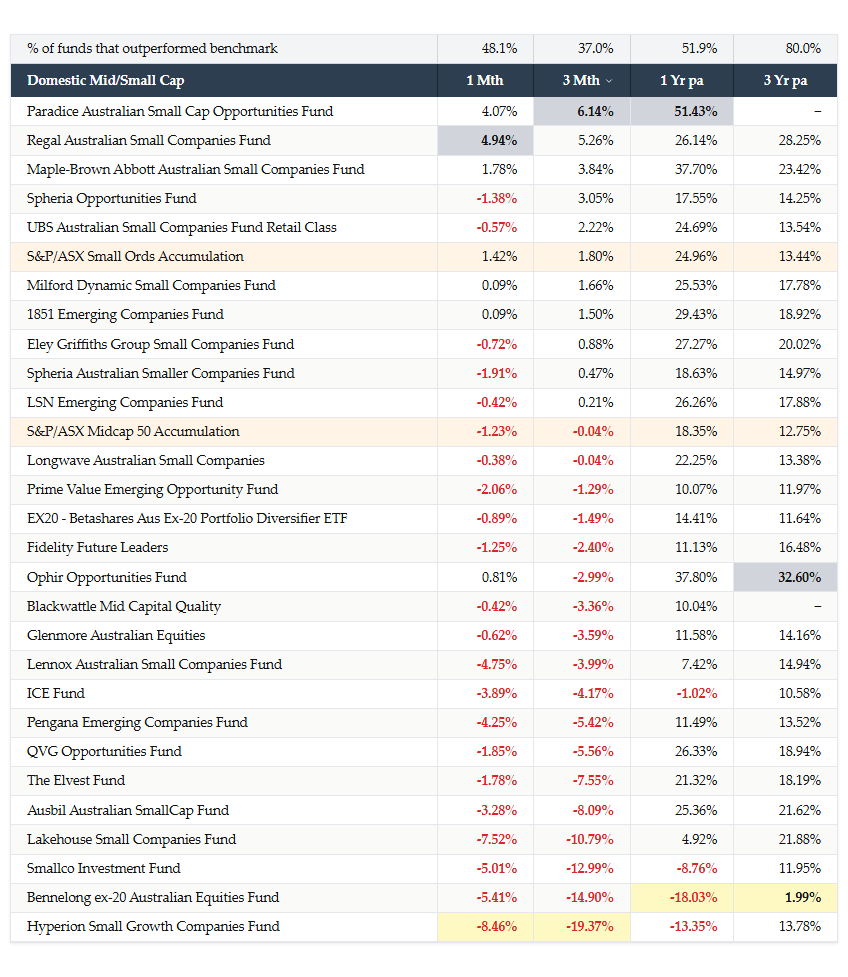

Domestic Mid/Small Cap

Concentration and mid-caps got slammed last month with a few large blow ups.

Some funds here have underperformed the benchmark by more than 35% over one year. At that level of underperformance, they’d need around +50% relative outperformance to get back to even.

Drawdowns are painful.

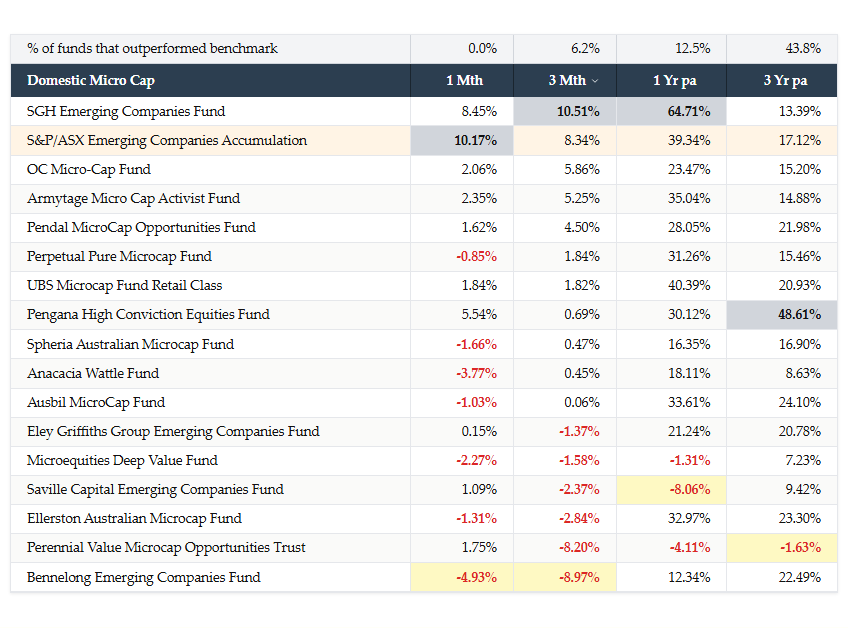

Domestic Micro Cap

If you didn’t hold lithium/gold/commodities in your fund, the benchmark ripped your face off.

Some stunning numbers and marketing teams finally starting to talk about the opportunity set here. imo a bit after the fact.t?

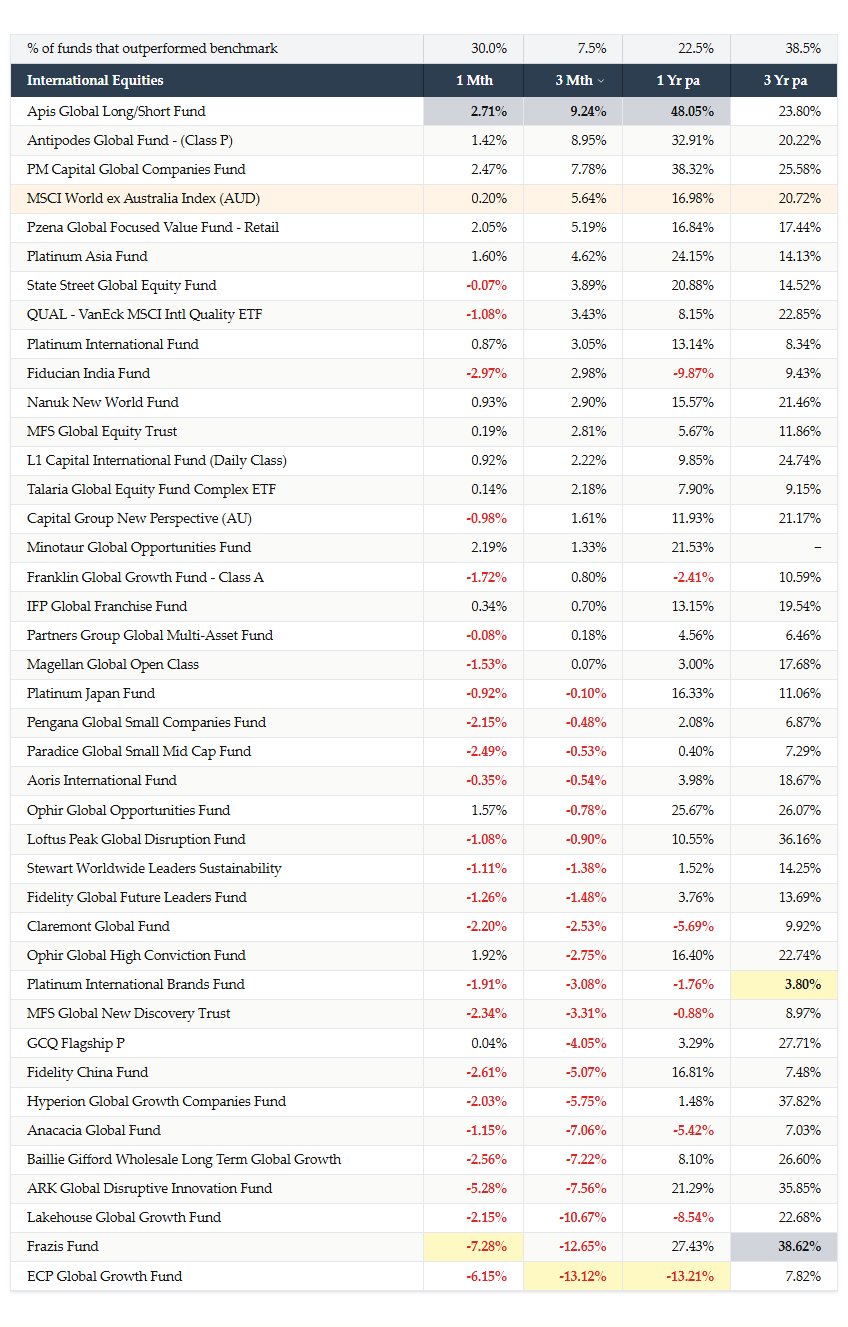

International Equities

Is this not insane? Less than 10% of funds outperformed their benchmark over the quarter. And the index continues to dominate overall.

The quality bubble continues to deflate.

I still find it fascinating that many funds are so deeply underweight tech & AI.

Furthermore I’m fascinated that most PMs I speak to about AI can talk about the technology yet barely use it themselves for anything other than notetaking.

Finally the thing that blows my mind is so many have mentioned that they are worried about llm models no longer improving and demand disappears.

Exponents do not stop dead! The bigger question is what if demand is so deeply underappreciated and the growth continues? A huge risk of omission.

SAAS businesses that drove the COVID tech bubble are dead in my view. Stock-based compensation means PE firms won’t touch them. And LLM progress is going to displace so many, why pay someone else when you can build internally?

This won’t happen overnight, but switching costs and build costs are fast approaching zero.

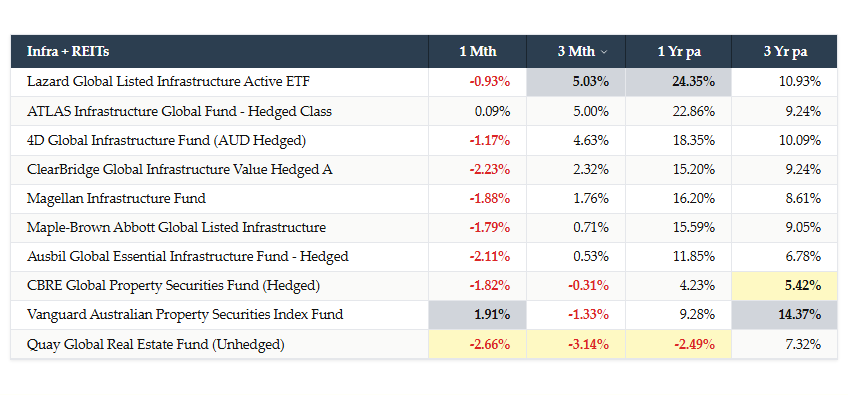

Infra + REITs

Real Estate exposure getting genuinely hit by bond curves moving higher, very difficult to express any kind of active management when correlations to yields are so high.

Infra does well nonetheless, real world assets deeply in demand and the space continues to attract the attention of both corporates and soverigns worldwide.

Listed infra has the “private infra put” where privatisation of listed infrastructure assets will occur at discounted prices.

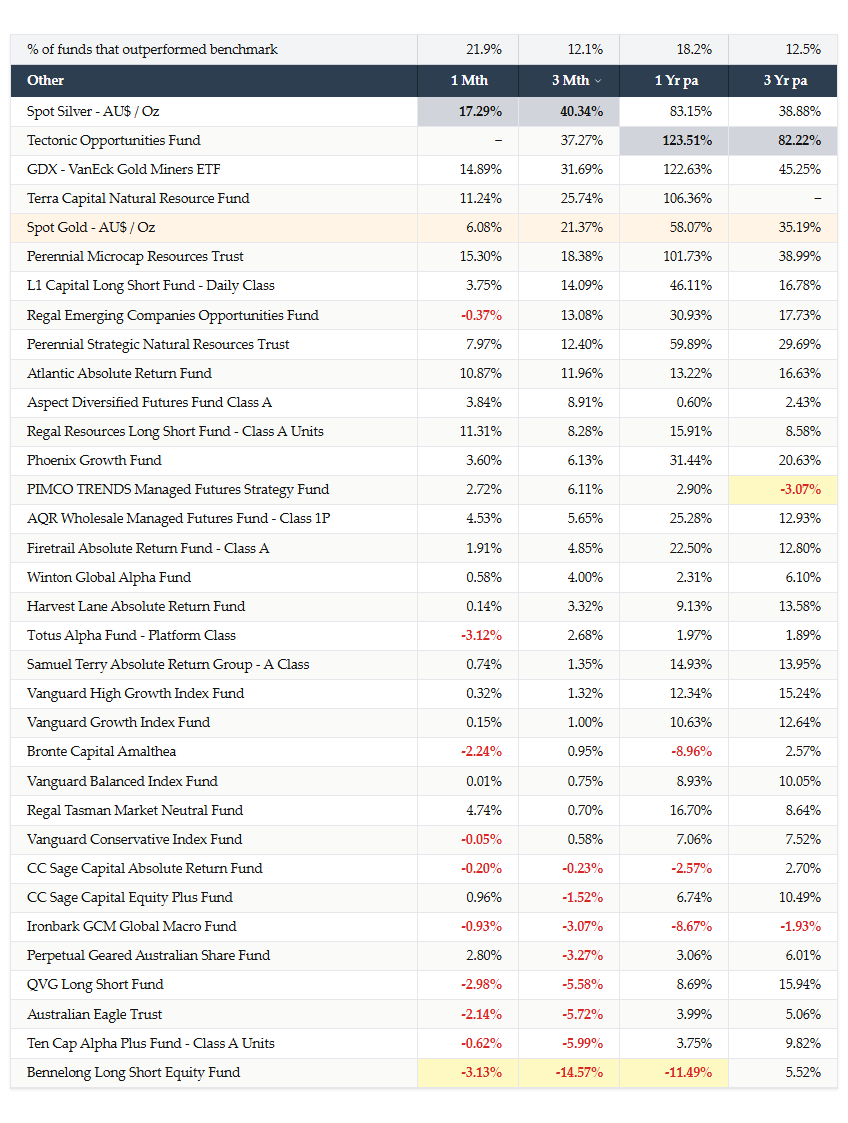

Other

GDX perfomance is insane, a triple in 3 years. With many funds tracking closely behind.

I keep banging on about this, but AQR are on an absolutely different level to the other Trend CTAs. How much equity risk though...

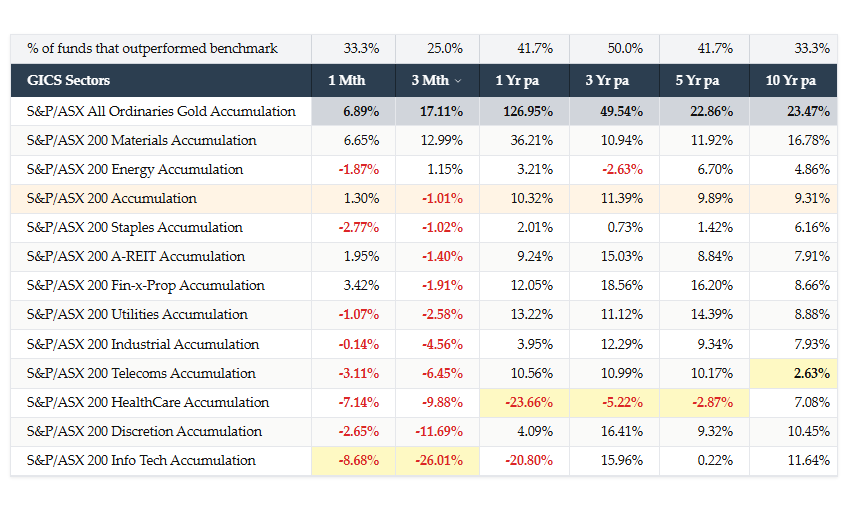

GICS Sectors

Gold continues to run higher and miners still aren’t that expensive. Ebbs and flows though, big runs like this will see institutional profit taking = opportunities for entry.

Copper finally getting the bid it deserves. Combined with Coal names running higher, Materials sector positioned well. AUD going to be a challenge.

Aussie tech running out of puff? Horrific year and gone no where over 5 years. But without any AI exposure this is standard, anything software related is getting pumped.

Your private SaaS val has been halved if you have any in your portfolio.

Crypto

Terrible month of anything crypto and finally a negative annual number, first time in 2 years.

The attention economy, why would retail allocate here when precious metals, AI & tech gets much more attention. Investors can get the same volatile exposure of crypto by investing in Silver or Sandisk for example today.

Remember this goes in cycles, so do not ignore.

Thanks

Well done for making it this far and it pleases me you are reading this sentence. I thank you for reading the above and I hope it has provoked some thoughts.