Allocating Capital

Let's talk about "Risk Free" Returns

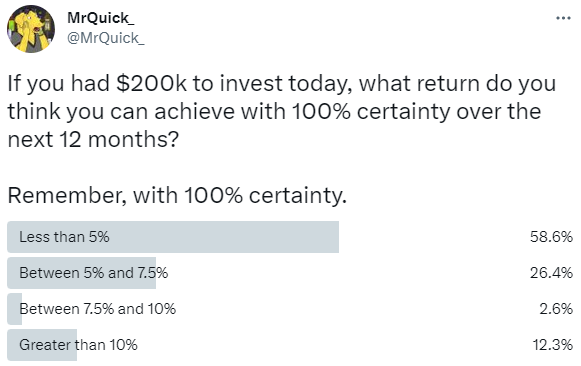

Thank you to all who answered the poll. It threw up some interesting results and some people got the point I was trying to make.

Results after 24 hours shown below:

(C’mon, greater than 10% is an ego response)

I could argue that as of today, only 2.6% of respondents guessed correctly. But the right answer is as always, “It Depends”.

This is less a poll about returns and more about capital allocation. It is a bit of a test for how we think about deploying cash in relation to income, tax and net outcomes.

Frame of Reference

Many of those who are managing capital today only started their careers post-GFC. I too was at Uni during the GFC and traded stocks frequently before I got the slap-down that was 2008. Truly a costly education.

For me and many others, our careers really started in the time of QE and our anchoring bias for rates is a cash rate of 3% or lower. Unless you travelled outside Australia to developing countries on a regular basis, no one has truly experienced what inflationary pressures are actually like in a very long time. The implications for allocating capital is gigantic.

Money is costly.

What is the right answer?

It is easy enough to talk about this on an institutional basis or in terms of allocating a pool of capital to investments. But what really matters is how you and I think about capital allocation on an individual level. We all just want to get ahead and get richer.

So, let’s forget about how we allocate capital theoretically and think about allocating capital in your own portfolio. If you are reading this, you are likely highly educated, have a good knowledge of financial markets, likely own your home with a mortgage against it. Your marginal tax rate is likely 32.5% or higher. I know a fair few who read this here get taxed at 45% for every incremental dollar they earn.

RBA cash rates continue to increase, with the recent lift by +25bps to 3.35%. You can get a cash savings rate of over 4% today at banks with various hurdles and conditions. And 12-month term deposit rates max out over 4% too.

So the answer is less than 5%? …Maybe. Maybe not.

I don’t think it is for the average Australian with a mortgage against their home.

(If you are a retiree, wealthy, don’t own your own home, etc, this really doesn’t apply to you)

What is your home loan rate today?

There is a wide range of interest rates for home loans and it is hard for me to pull a number out of the air. But let’s make it easy for this discussion. Very simply I am going to assume banks will earn 190bps of Net Interest Margin over the RBA cash rate, therefore I am simply going to extrapolate:

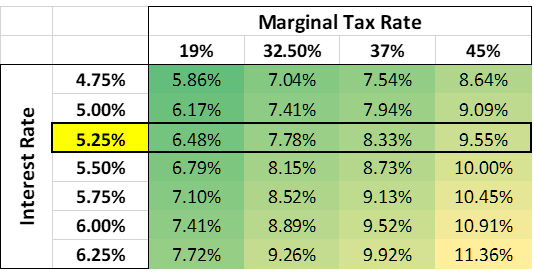

Therefore Average Loan Interest is <3.35%+1.90%> = 5.25%.

Please note that this is for Owner Occupied, Principal and Interest mortgages. NOT investment loans or interest only or margin loans. Purely the mortgage on a principal place of residence. The roof over your head.

As a reminder, my question becomes about allocating the additional $200k to the most efficient use where you can maximise the return with a high level of certainty. (Nothing is ever certain, not even interest rates!)

The table above shows what pre-tax investment return you need to achieve at the very minimum at the various tax rates to make it worthwhile investing instead of paying down your mortgage.

At the current rate (I am assuming 5.25% today as highlighted above), you need to achieve a minimum pre-tax return of:

7.78% if you earn between $45k-$120k per annum

8.33% if you earn between 120k-180k per annum

9.55% if you earn more than $180k per annum

What is your home loan rate tomorrow?

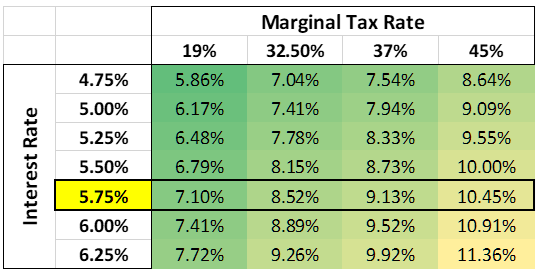

Looking forward, on average the RBA cash rate is expected to hit approx. 3.90%1 at some point this year. Using our little equation shown above leads to an Average Loan Interest of 5.80%. Let’s round to 5.75% to show this in the table again:

So once again, if the average loan rate on home loan is 5.75%pa assuming the RBA increases the cash rate to 3.90%, you need to achieve a minimum pre-tax investment return of:

8.52% if you earn between $45-$120k per annum

9.13% if you earn between 120-180k per annum

10.45% if you earn more than 180k per annum

10.45%!!!

For anyone at the highest marginal tax rate, if rates continue to increase, I can argue that you need to generate a “risk-free” return of greater than $21,000 on the $200,000 available to deploy in any investment before it makes financial sense to do so.

Once again, I want to frame this in everyone’s perspective of managing their lives. It is not easy to generate a return great than 10% per annum. In fact, I’d even go as far as saying it is difficult.

Cost of Capital and Equity Risk Premia

How do we think about cost of capital when making new investments in this lens?

From what I’ve clearly shown above, does that mean we need a 10% hurdle for any new investments? …Maybe.

From my perspective, and ignoring the craziness that was the falling-rate environment of the last decade, allocating capital to risk actually does deserve to earn a premium over the risk-free rate. Simple stuff really.

There is plenty of data and research available on equity risk premium (ERP) that I am not going to bother quoting at this stage (but if you want please let me know), but ERP is commonly taken to be circa 5.50% above the risk-free rate of return.

If we end up at 3.90% terminal cash rates and as a taxpayer at the highest marginal tax bracket, the required return is 10.5% (pre-tax rF) + 5.50% (ERP) = 16%.

I think that makes sense, why should you be getting out of bed for anything less than 16% for taking on equity risk in todays environment?2

This has implications for equity markets and allocating capital if you are trying to pay off your mortgage. Desired equity returns are perhaps different for those who are wealthier and don’t have the added stresses of mortgages and debt but the surely you would think that there is some consistency between various groups of individuals as taxes are always certain.

A Tidal Force

The rising tides that was falling interest rates have abated for now and one might need to be a bit smarter about allocating capital these days. Money is costly and it is hard to continue underwriting pre-tax equity returns at the historical returns of the ASX200.

So where does capital get allocated in the future? Should we be seeing a major deleveraging event across markets? Maybe, but I don’t think so as simply not enough people are aware of what I’ve covered here or are aware of the mechanics of it all.

The final question I leave you with is to think about how these numbers interact with inflation and real returns, they really do throw a real (haha) spanner in the works.

Formalities

While I take care to make sure stuff I say and the data is correct, I do not make any guarantees as to the complete accuracy of these figures. The data and comments above are simply my observations and not financial advice.

Seriously, this is not financial advice and simply more a summary of my most recent thoughts on how I am thinking about deploying my own capital as a man with a lot of debt.

I’m not making a prediction, but simply using implied curve available from the ASX. The 3.90% I have quoted is per as at 6 Feb 2023. But please check here as it changes everyday.

This does lead me to a bone I need to pick. I keep seeing many companies (largely resource companies!) who use unrealistic cost of capital assumptions in their calculations for NPV & IRR. When you see someone quote NPV5 or NPV8, it is deceitful and disingenuous. Who even quotes NPV5 numbers when you can’t even borrow at 5% these days! I still see brokers using NPV8 numbers still, are you kidding me!?!